Best Pine Script Strategy Tester Guide for Effective Trading Strategy Testing

Backtesting is a crucial process in trading that allows traders to evaluate the viability of their strategies using historical data. In this guide, we will delve into Pine Script, TradingView's proprietary scripting language, to help you backtest your trading strategies effectively. This article will cover everything from the basics of Pine Script to advanced backtesting techniques, ensuring you have a solid understanding of how to leverage this powerful tool.

What is Pine Script?

Pine Script is a domain-specific programming language created by TradingView for developing custom technical indicators and strategies. It is designed to be user-friendly, allowing traders and developers to write scripts with relatively few lines of code compared to other programming languages.

Key Features of Pine Script

- Simplicity: Easy to learn for those familiar with programming concepts.

- Integration: Directly integrates with TradingView’s charting tools.

- Customizability: Users can create unique indicators and strategies tailored to their trading styles.

Why Backtest Your Strategies?

Backtesting provides several advantages:

- Validation: Helps validate the effectiveness of a trading strategy before risking real capital.

- Optimization: Allows traders to refine their strategies by analyzing past performance.

- Risk Management: Aids in understanding potential drawdowns and risk exposure.

Getting Started with Backtesting in Pine Script

To begin backtesting in Pine Script, follow these steps:

- Open TradingView: Navigate to TradingView and log in or create an account.

- Access Pine Editor: Click on the "Pine Editor" tab at the bottom of the screen.

- Write Your Strategy: Use the

strategy()function to define your trading strategy.

Basic Structure of a Pine Script Strategy

Here’s a simple example of a moving average crossover strategy:

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Pineify

//======================================================================//

// ____ _ _ __ //

// | _ \(_)_ __ ___(_)/ _|_ _ //

// | |_) | | '_ \ / _ \ | |_| | | | //

// | __/| | | | | __/ | _| |_| | //

// |_| |_|_| |_|\___|_|_| \__, | //

// |___/ //

//======================================================================//

//@version=6

strategy("[Pineify - Best Pine Script Generator] Simple MA Crossover", overlay=true)

shortMA = ta.sma(close, 10)

longMA = ta.sma(close, 30)

if (ta.crossover(shortMA, longMA))

strategy.entry("Long", strategy.long)

if (ta.crossunder(shortMA, longMA))

strategy.close("Long")

![[Pineify - Best Pine Script Generator] Simple MA Crossover - Chart](https://r2.pineify.app/assets/42dabb26cd182d33b086367ce51b40ad.png)

1. Defining Entry and Exit Conditions

The core of any backtesting script is defining when to enter and exit trades. This is done using conditional statements that trigger buy or sell orders based on specific criteria.

2. Customizing Backtesting Range

To backtest over a specific date range, you can add input parameters for start and end dates. Here’s how:

fromYear = input(defval=2020, title="From Year")

toYear = input(defval=2021, title="To Year")

startDate = timestamp(fromYear, 1, 1, 0, 0)

endDate = timestamp(toYear, 12, 31, 23, 59)

timeCondition = (time >= startDate) and (time <= endDate)

Incorporate this condition into your entry logic:

if (ta.crossover(shortMA, longMA) and timeCondition)

strategy.entry("Long", strategy.long)

3. Viewing Results in Strategy Tester

Once you have written your script, add it to your chart by clicking “Add to Chart.” Then access the Strategy Tester at the bottom panel to view performance metrics such as:

- Total Net Profit

- Maximum Drawdown

- Percentage of Profitable Trades

![[Pineify - Best Pine Script Generator] Simple MA Crossover - Result](https://r2.pineify.app/assets/031d1f6695e82fe1cd431f61db814903.png)

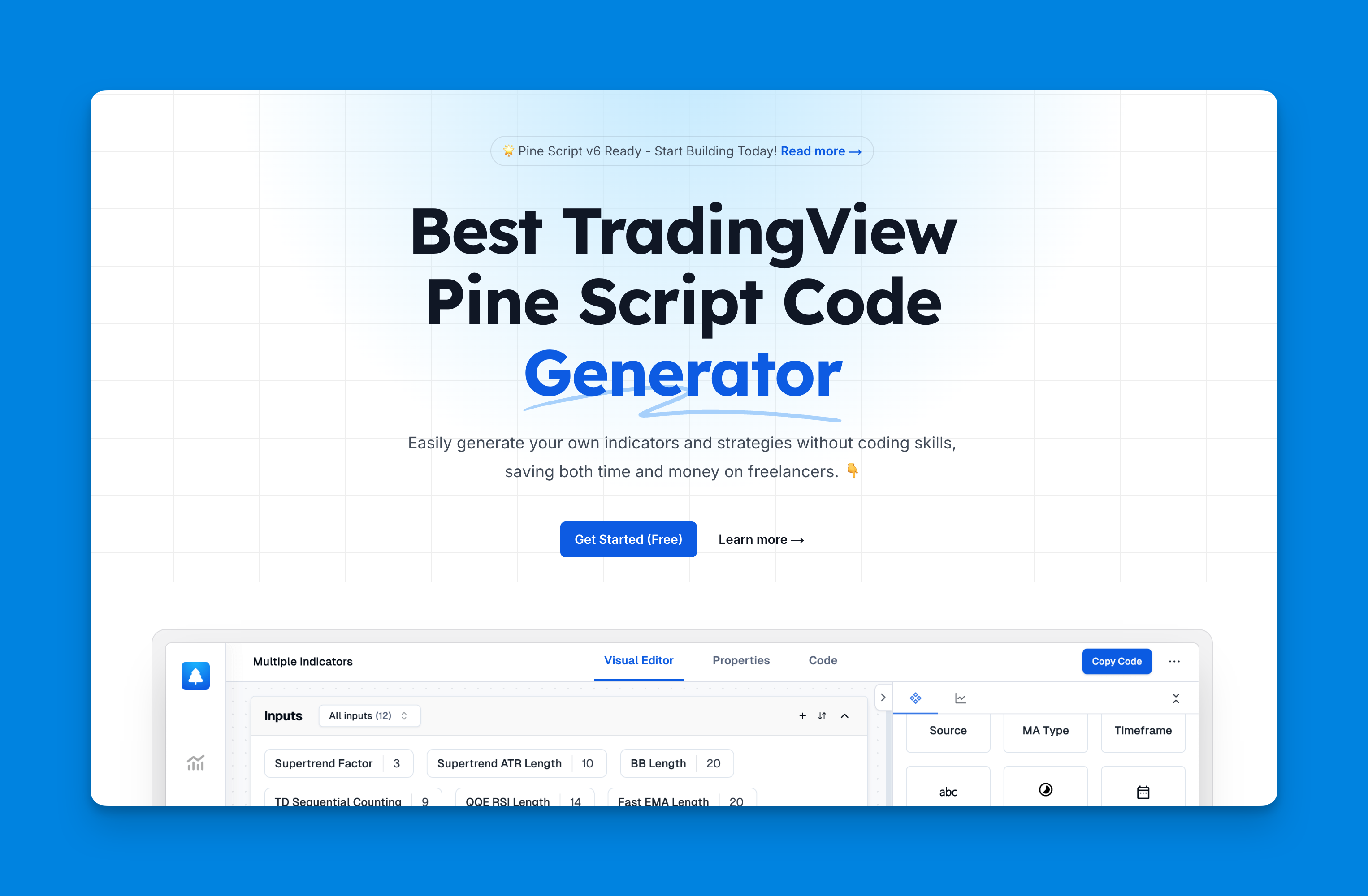

Using Pineify to Generate Pine Script Strategy Code

Website: Pineify

Pineify is a free Pine Script code generator that simplifies strategy development. Its user-friendly interface allows traders to create and customize indicators without writing code, making it accessible for users of all skill levels.

The platform features a powerful condition editor for combining technical indicators and price data. Users can backtest generated scripts in TradingView and add unlimited indicators to their charts, making it a cost-effective solution compared to hiring developers.

At Pineify, you can customize your trading strategy based on conditions or indicator signals.

![[Pineify - Best Pine Script Generator] - Add Strategy Entry](https://r2.pineify.app/assets/a81c5a1c9bac50b08afcb9dc6ac7d976.png)

Click here to view all the features of Pineify.

Advanced Backtesting Techniques

Deep Backtesting

TradingView has introduced a Deep Backtesting feature that allows users to analyze strategies over extended historical periods beyond the default limits. To utilize this feature:

- Enable "Deep Backtesting" in the Strategy Tester settings.

- Specify your desired date range.

This feature significantly enhances the robustness of your backtests by providing more data points for analysis.

Incorporating Risk Management

Effective backtesting should include risk management techniques such as stop-loss orders and position sizing. Here’s an example of adding a stop-loss:

stopLossLevel = close * 0.98 // Stop-loss at 2% below entry price

if (ta.crossover(shortMA, longMA) and timeCondition)

strategy.entry("Long", strategy.long)

strategy.exit("Exit Long", "Long", stop=stopLossLevel)

Common Pitfalls in Backtesting

- Overfitting: Tailoring a strategy too closely to historical data can lead to poor performance in live trading.

- Ignoring Slippage and Commissions: Real-world trading incurs costs that should be factored into backtests for accuracy.

- Inadequate Data Range: Testing over too short a period may not provide reliable results.

Conclusion

Backtesting using Pine Script on TradingView is an essential skill for traders looking to validate their strategies before live implementation. By following the steps outlined in this guide and leveraging advanced techniques like deep backtesting and risk management, you can significantly enhance your trading performance.

References:

- https://quantnomad.com/backtesting-pine-script-strategies-on-entire-history-with-deep-backtesting/

- https://www.reddit.com/r/TradingView/comments/12ftwp0/backtesting_with_pinescript/

- https://stackoverflow.com/questions/69321468/backtesting-in-pine-script

- https://algotrading101.com/learn/pine-script-tradingview-guide/

- https://quantnomad.com/faq-how-to-insert-backtesting-range-to-pinescript-strategies/

- https://optimusfutures.com/blog/how-to-backtest-on-tradingview/

- https://www.youtube.com/watch?v=gpfN_18h2D4

- https://www.youtube.com/watch?v=o2yKotJ-6cw

- https://www.tradingview.com/pine-script-docs/v4/essential/strategies/

- https://quantra.quantinsti.com/glossary/How-to-Backtest-Trading-Strategies-in-Pine-Script